课程简介

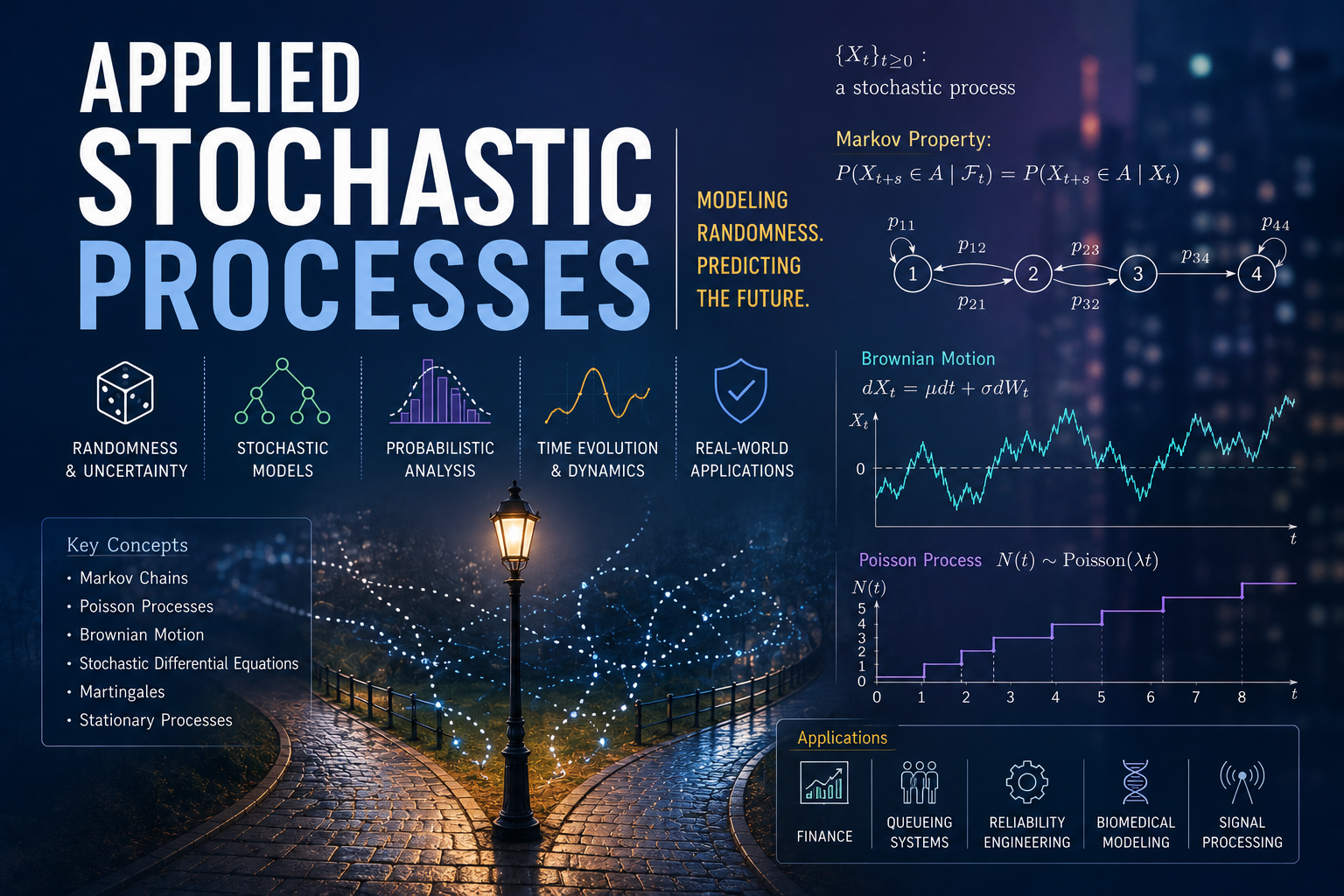

This course provides a rigorous introduction to stochastic processes, with emphasis on the

structure and analysis of Markov processes. It begins with a brief review of fundamental

concepts in probability, including conditioning and limit theorems. The course then develops key

classes of stochastic processes, including Poisson processes, renewal and regenerative processes,

and both discrete-time and continuous-time Markov chains. Hidden Markov models on finite

state spaces are also introduced. Throughout the course, attention is given to both theoretical

foundations and practical modeling considerations, with applications drawn from queueing

systems, finance, and related areas.